How to Automate Your Savings Without Feeling Broke

Sarah Johnson

17 March 2026

How to Automate Your Savings Without Feeling Broke

Introduction

Imagine building wealth while you sleep, eat, and go about your daily life – all without the constant mental strain of deciding whether to save or spend. Automated savings can transform your financial future, but here’s the catch: most people set it up wrong and end up feeling financially squeezed.

The key isn’t just automating your savings; it’s doing it strategically so you barely notice the money leaving your account. When done correctly, automated savings becomes a invisible wealth-building machine that works in the background of your life.

In this comprehensive guide, we’ll explore psychology-backed methods to automate your savings without sacrificing your quality of life or leaving you scrambling for cash at month’s end.

The Psychology Behind Painless Automated Savings

Understanding the mental aspects of saving is crucial for long-term success. Behavioral economics shows us that our brains are wired to resist loss – even when that “loss” is actually beneficial saving.

The Pain of Paying Principle

Research by behavioral economist Dan Ariely reveals that we experience genuine psychological pain when parting with money. This “pain of paying” is why many savings attempts fail – our brains literally fight against the process.

The solution? Make savings invisible and automatic so your brain doesn’t register the “loss.”

Mental Accounting Magic

People naturally create mental “buckets” for different types of money. By leveraging this tendency, you can:

- Separate savings from spending money mentally

- Create specific savings goals that feel rewarding

- Use the “pay yourself first” principle effectively

- Track your actual expenses for 30 days

- Identify your true necessities vs. flexible spending

- Find your “comfort threshold” – the minimum amount you need to feel secure

- Builds the habit without financial stress

- Proves the system works

- Creates momentum for larger amounts

- Month 1-3: 2% automated

- Month 4-6: 3% automated

- Month 7-9: 4% automated

- Continue until you reach 15-20%

- Target: 3-6 months of expenses

- Automation: $100-300 monthly (adjust based on income)

- Access: High-yield savings, easily accessible

- Target: Vacation, car down payment, home repairs

- Automation: Variable based on timeline

- Access: Money market or short-term CDs

- Target: Retirement, investment opportunities

- Automation: 10-15% of income

- Access: 401(k), IRA, investment accounts

- Target: Guilt-free spending on wants

- Automation: 5-10% of income

- Access: Checking account for easy spending

- Money is available when transfers occur

- You “pay yourself first” before other expenses

- Remaining money feels like your true spending budget

- Apps like Acorns or Qapital round purchases to the nearest dollar

- Spare change automatically goes to savings/investments

- Typical savings: $50-200 monthly

- Save a small percentage of every transaction

- Set rules like “save 10% of any purchase over $20”

- Creates variable but consistent savings

- Pros: Savings automatically increase with raises

- Cons: May decrease during lean months

- Best for: People with variable income

- Tax refunds

- Bonuses

- Cash gifts

- Side hustle income

- Review subscriptions and cancel unused services

- Redirect one small expense (daily coffee, streaming service) to savings

- Use cashback from credit cards or apps

- Use accounts at different banks to create friction

- Set up savings accounts without debit cards

- Create a 24-hour rule before touching savings

- Base automation on your lowest monthly income

- Use percentage-based rules instead of fixed amounts

- Create a “smoothing account” to even out income fluctuations

- Setup time: 5-10 minutes online

- Cost: Usually free

- Flexibility: Easy to modify amounts and timing

- Higher interest rates than traditional banks

- Easy automation setup

- FDIC insured

- Automatic investing in diversified portfolios

- Rebalancing and tax optimization

- Lower fees than traditional financial advisors

- Connect all accounts for comprehensive view

- Automated categorization and tracking

- Savings goal monitoring

- Savings Rate: Percentage of income automatically saved

- Account Growth: Monthly increase in savings balances

- Goal Progress: How close you are to specific targets

- Automation Efficiency: Percentage of savings that’s automated vs. manual

- Use apps that show progress bars for goals

- Create charts showing account growth over time

- Celebrate milestones with small rewards

- Monthly 15-minute “money dates” with yourself

- Quarterly automation adjustments

- Annual goal setting and strategy review

- Start small and increase gradually

- Automate immediately after payday

- Use multiple accounts for different goals

- Leverage technology to make it effortless

- Track progress to stay motivated

- Calculate 2% of your monthly income and set up one automatic transfer

- Open a high-yield savings account if you don’t have one

- Schedule a calendar reminder for three months from now to increase your savings rate

“The best time to plant a tree was 20 years ago. The second best time is now.” – Chinese Proverb

This wisdom applies perfectly to automated savings – the best time to start was yesterday, but today is your second chance.

Strategic Automation: The 50/30/20 Method Enhanced

The traditional 50/30/20 budgeting rule (50% needs, 30% wants, 20% savings) provides a solid foundation, but we can optimize it for painless automation.

Step 1: Calculate Your True Take-Home

Before automating anything:

Step 2: Start Small and Scale

Begin with just 1-2% of your income automated to savings. This might seem insignificant, but it serves crucial psychological purposes:

Step 3: The Ladder Approach

Increase your automated savings by 1% every three months:

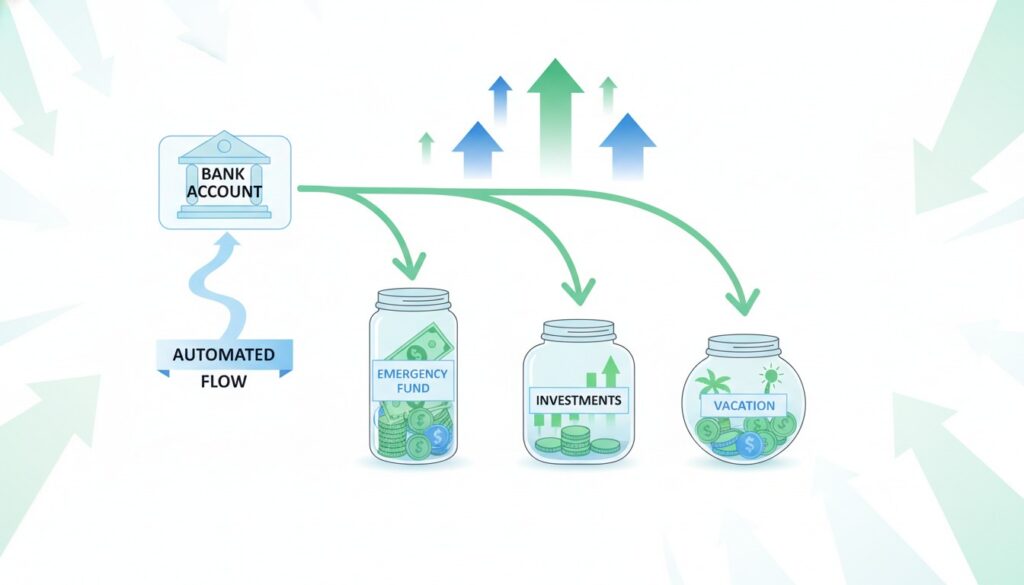

Multiple Account Strategy for Maximum Effectiveness

Using multiple savings accounts creates psychological separation and prevents you from “borrowing” from your future self.

The Four-Account System

1. Emergency Fund Account

2. Short-term Goals Account

3. Long-term Wealth Building

4. Fun Money Account

Timing Your Transfers

Set all automated transfers for 1-2 days after payday. This ensures:

Advanced Automation Techniques

The Micro-Savings Revolution

Modern fintech apps offer innovative ways to save without thinking:

Round-up Programs

Percentage-based Automation

Income-based Scaling

Set up percentage-based transfers rather than fixed amounts:

The Windfall Strategy

Automate savings from unexpected money:

Overcoming Common Automation Obstacles

“I Don’t Earn Enough to Save”

Reality check: Even $25 monthly becomes $300 yearly, plus compound interest. Start with what you can afford, even if it’s just $10 monthly.

Action steps:

“I Keep Spending My Savings”

Solutions:

“My Income is Too Irregular”

Strategies for variable income:

Technology Tools and Apps

Traditional Banking Automation

Most banks offer free automatic transfer services:

Savings Apps and Platforms

High-yield Savings: Marcus, Ally, Capital One 360

Investment Automation: Betterment, Wealthfront, M1 Finance

Budgeting Integration: Mint, YNAB, Personal Capital

Measuring Success and Staying Motivated

Key Metrics to Track

Motivation Strategies

Visual Progress Tracking

Regular Reviews

“A budget is telling your money where to go instead of wondering where it went.” – Dave Ramsey

Conclusion

Automated savings doesn’t have to mean financial hardship or constant money stress. By understanding the psychology behind spending and saving, implementing gradual increases, and using the right tools and strategies, you can build substantial wealth while maintaining your quality of life.

Remember these key principles:

Take Action Today

Don’t let this information become just another article you read and forget. Your future self is counting on the decisions you make today.

Start with these three actions:

What’s your first step going to be? Your future financially secure self will thank you for taking action now.